Published Jan 22, 2020 by A.J. Mistretta

Partnership 2020 Board Chair Bobby Tudor, Chairman of Tudor, Pickering, Holt & Co. LLC, discussed priorities for the year ahead, specifically how the Partnership will work to address energy transition, at the organization's Annual Meeting on January 22.

It is a great honor and privilege to step into this role as chair. I am very much looking forward to our work together.

As Bob alluded to a moment ago, I want to talk about the concept of an Energy Transition; and what that may mean to business in Houston.

The economic vitality and growth of our region’s economy is inextricably tied to the Energy Industry. Around the globe, Houston is known and revered for being the world capital of this mission-critical industry.

Detroit and Automobiles.

Silicon Valley and High Technology.

New York City and Finance.

Los Angeles and Entertainment.

Houston and Energy.

It’s big. It’s complicated. It sits at the intersection of science, technology, economics and geopolitics. It touches every single nook and cranny of the global economy, in ways that most people take completely for granted.

And notwithstanding what we hear from some corners of media and politics, it has been a force for good in the world. The demonization of the energy business is hypocritical and just plain wrong. It is not helpful to finding a path to a cleaner future.

The energy business is also changing, and as in most other areas of the global economy, that change is coming at a rapid pace.

As business leaders and members of the Greater Houston Partnership, it’s our job to look around corners and anticipate both cyclical and secular change.

And with that anticipation, to position our local economy to thrive and grow, creating opportunity for All Houstonians.

So, what will that change look like? What IS the so-called “Energy Transition”? How does this relate to combating climate change? And what should we do about it?

In getting at some answers to those questions, I’d like to focus on four key thoughts.

#1: The Energy Industry has been very, very good to Houston.

#2: Oil and Gas production and consumption are not disappearing anytime soon; but….

#3: The traditional Oil and Gas business is not likely to be the same engine for growth in Houston for the next 25 years, that it’s been in the past 25 years. And…

#4: As Houston business leaders, we have both an opportunity and a responsibility to lead the transition to a cleaner, more efficient and more sustainable, lower carbon world.

Let’s start with the first thought.

While much has been said lately regarding the diversification of Houston’s economy, we all know that the central driver to the emergence and establishment of Houston as a leading global commercial and cultural center, is the energy sector.

Houston is the global brain trust of the industry:

• 4,600 Energy companies are located in Greater Houston

• Over 1/3 of Houston’s GDP comes from the industry

• 250,000 workers are DIRECTLY employed in the industry, with multiples of that being indirectly employed

• Average energy industry compensation is $140,000 per year, more than double the broader Houston average and positioning Houston as a national leader in GDP per capita

• Of Houston’s 21 Fortune 500 companies, 18 are energy companies

I’m not just talking oil & gas – it’s all segments of the value chain. Consider that:

• More than half of the world’s 100 largest chemical companies have operations in greater Houston

Not only is Houston the brain trust, it is also the arterial system of the global energy industry:

• Houston companies control 54% of US Natural Gas pipeline capacity, and 32% of US oil pipeline capacity

• The Houston Ship Channel industrial complex is the largest of its type in the world

If anything, these data points probably understate the importance of the energy industry to our economy and our life here in Houston.

If you own a restaurant, or a law firm, or a clothing retailer, or a travel agency – the health and vitality of the energy industry matters to your business and to your community—and in all probability, it matters more than you know.

It’s a key driver of most everything—including the philanthropy that has given us first class cultural institutions, universities, parks, and healthcare. Of the 20 largest United Way campaigns, 11 are energy companies. The wealth generated by the industry has been widely impactful in our city.

The industry has been very, very good to Houston and we all owe a debt of gratitude to the risk -takers, entrepreneurs, leaders, scientists, workers and capital providers who have made it all happen. It’s a stunning accomplishment.

Now to my second point: Oil & Gas is not going away anytime soon.

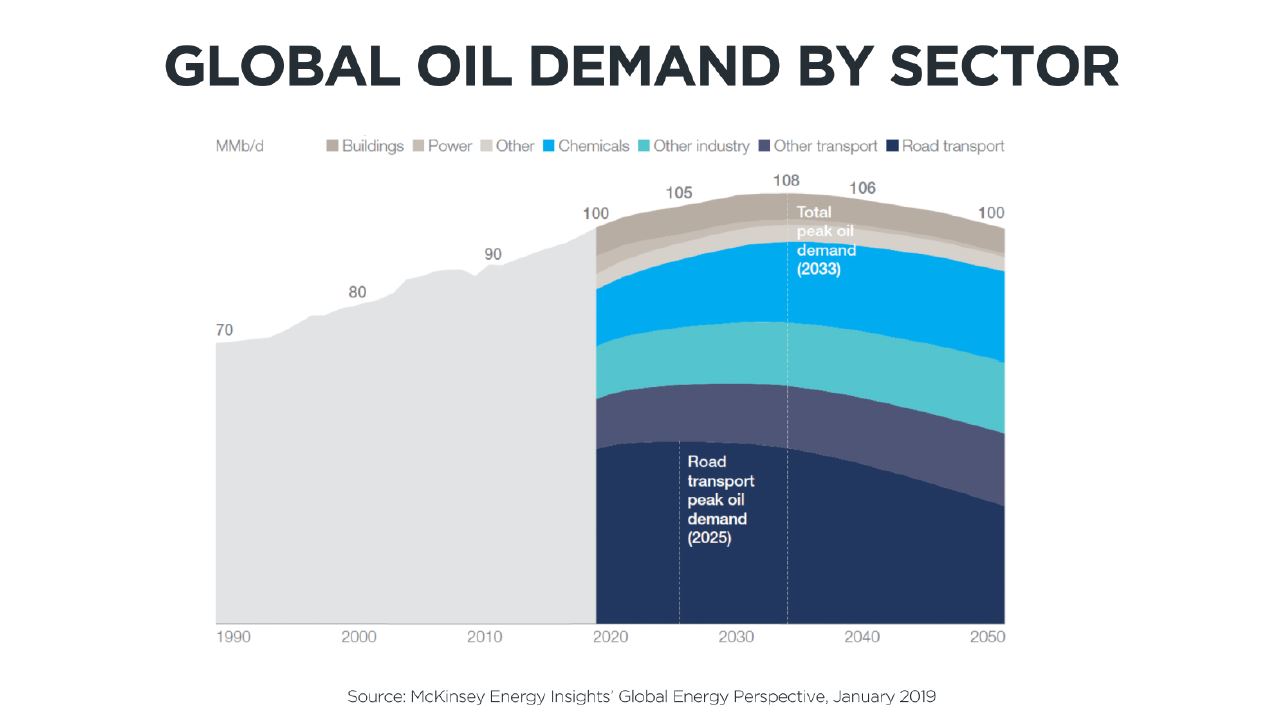

While this idea may be contested by some, even the most ardent advocates for an abrupt transition away from fossil fuels will admit that it is likely that, absent some unexpected technological breakthrough in battery and other industrial technology, global demand for fossil fuels will continue to grow for another 15 to 20 years.

This slide here from McKinsey shows that growth to a peak in the middle of next decade, leveling out and then a slow decline.

Importantly, I should point out, we likely will be consuming as much oil globally in 2050, as we are today.

In short, in order to avoid massive economic disruption and hardship, especially in the developing world, we will need to continue to produce and consume large amounts of hydrocarbon-based fuels, for many decades to come.

Without it, the world’s poor will not climb out of poverty.

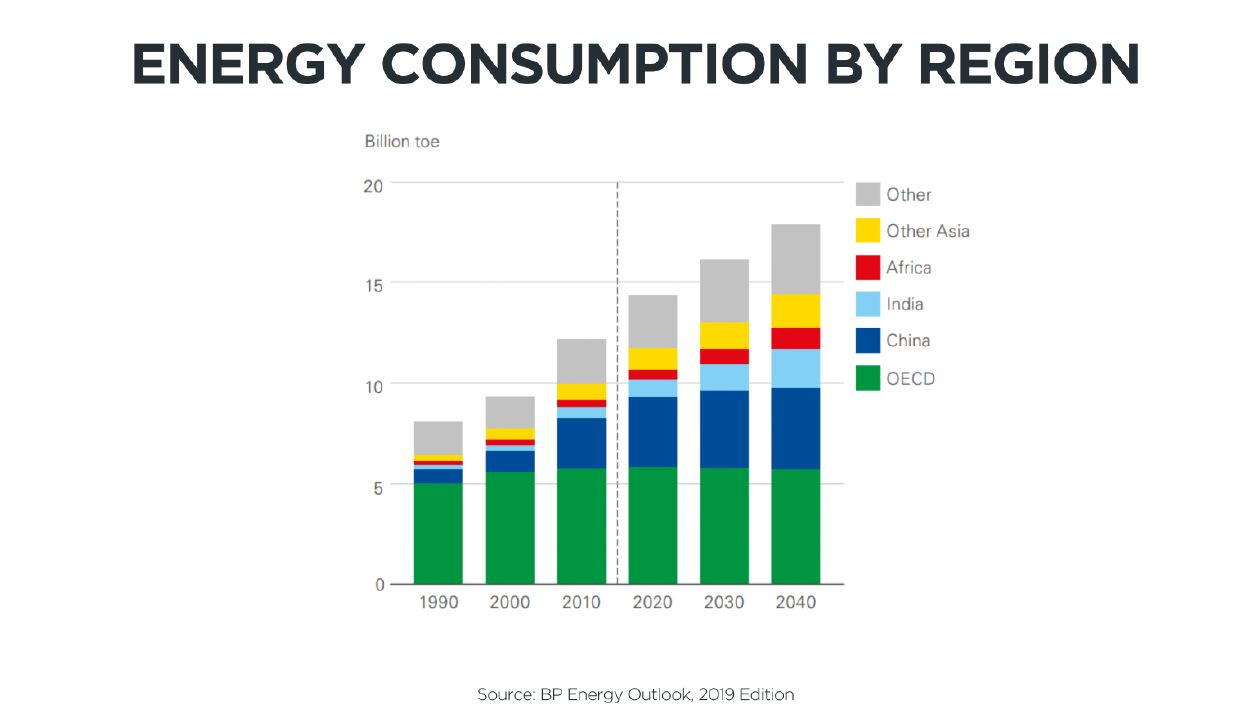

According to BP’s Global Energy Outlook shown on the screen, in 1990, the OECD accounted for almost two-thirds of global energy demand; the developing world just one-third. By 2040, that has completely flipped with emerging economies accounting for over two-thirds of demand.

So, we know demand for affordable, reliable energy will continue to grow.

And I noted that absent a breakthrough, oil and gas is not going away anytime soon.

So, that begs the questions…“what is ‘anytime soon’,” and “what if we do have major technological breakthroughs?”. In the overall scheme of things, 15 to 20 years is not a very long time, and technology is advancing rapidly.

How do we know that major disruption isn’t coming sooner?

And, oh by the way, what about Climate Change?

Which leads us to my third point:

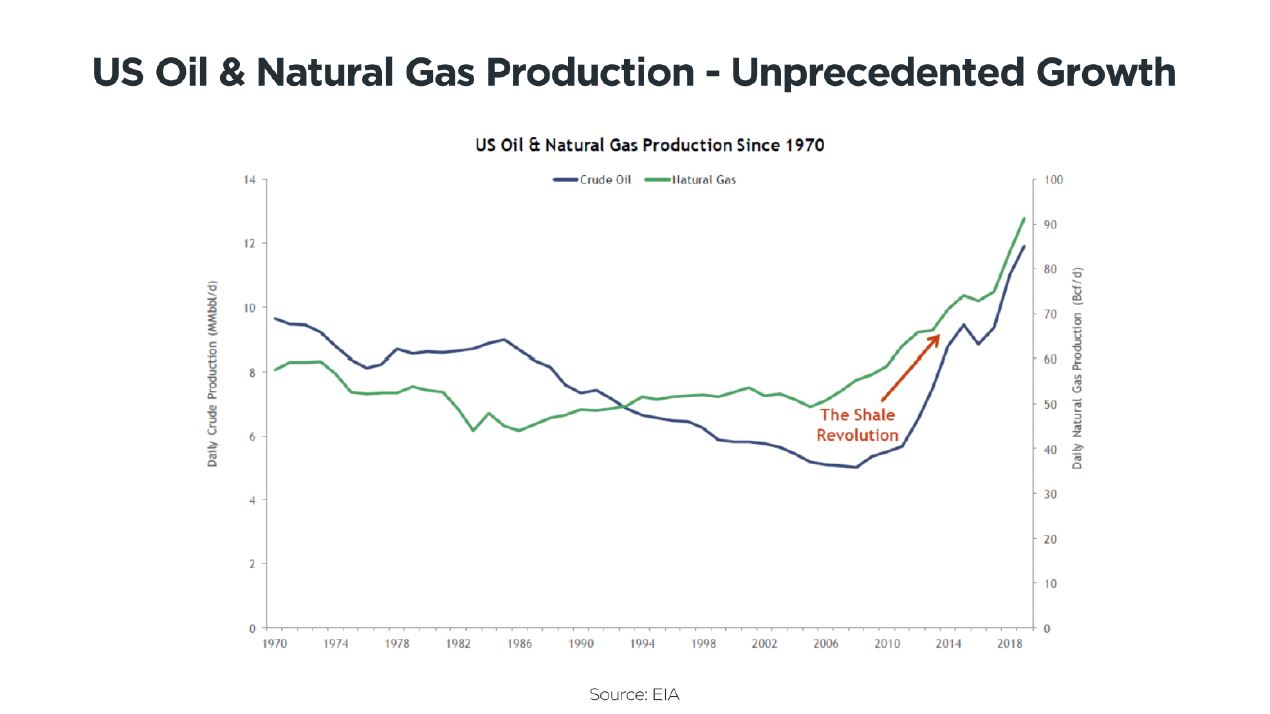

The Oil and Gas business is not likely to be the same engine for Houston’s growth over the next 25 years, that it’s been in the past 25 years.

As a reminder, these past 25 years saw a revolution in the industry; “The Shale Revolution."

You can see the effects of that on this chart that shows U.S. oil production since 1970.

Thanks to our own George Mitchell, and our enterprising Oilfield Service industry, the shale code was cracked, making heretofore uneconomic quantities of oil and gas, suddenly not just economic, but among the lowest cost reserves in the world.

This technological achievement turned the global oil and gas industry on its head, making the US a net exporter of hydrocarbons; giving the US petrochemical industry a huge feedstock cost advantage, and turning Houston into the fastest growing major metro area in the United States.

In short, we became a boom town again.

But I have a former boss who used to say, “When something feels too good to be true, it usually is”, and sure enough, the shale-driven growth cycle hit a pothole or two. Let’s talk about those.

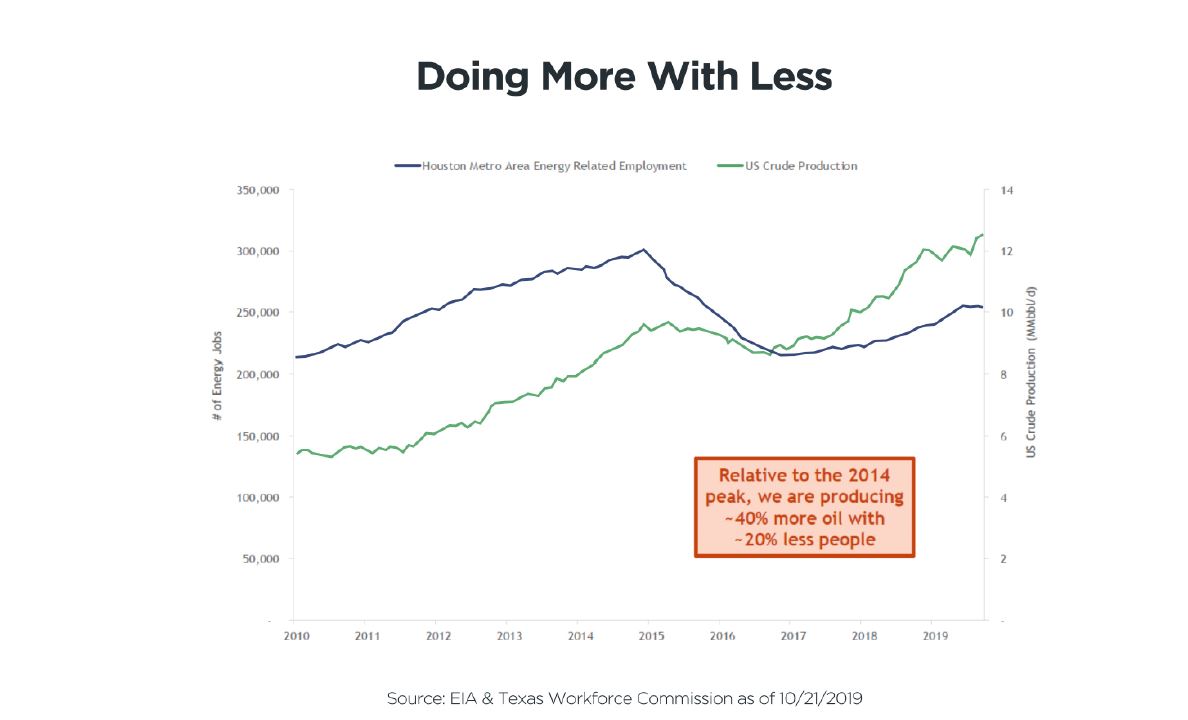

While we were growing, through technological advancement, we became even more efficient. This first line plots Houston area energy related employment. You can see the peak there in early 2015 and then a sharp decline.

We’ve been building back up, but quite slowly. In fact, we are still about 50,000 jobs off the high.

Now, let’s add this line – this shows U.S. Oil & Gas Production. It continues to grow at a high rate.

Simply put, we are creating more with less: 40 percent more oil production, with 20 percent less people. That trend is likely to continue, even as production grows.

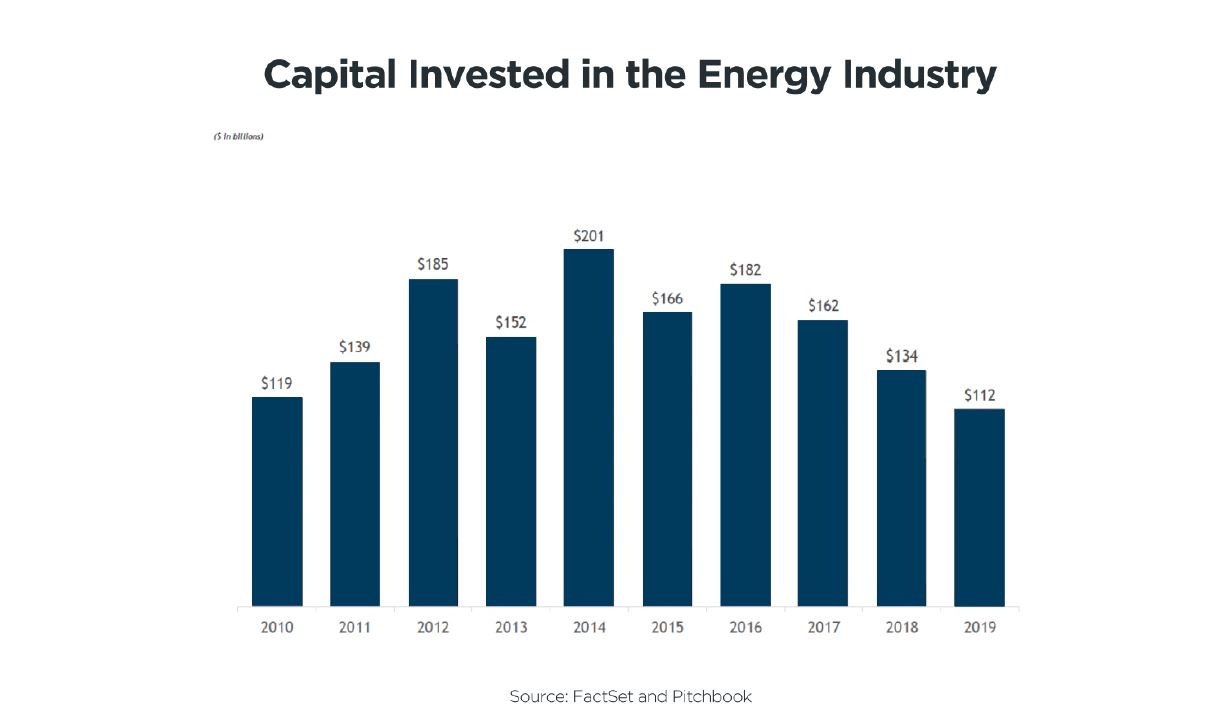

Secondly, the life blood of the energy industry is capital, and the industry historically consumes a huge amount of it. This chart shows the amount of capital invested in the U.S. energy industry since 2010.

You can see it peaking in 2014, and pulling back significantly.

One thing to understand, is that those capital providers “don’t do it for practice”, as they say. They are looking for returns, and if you don’t give them returns, they quit giving you capital. And that’s exactly what happened.

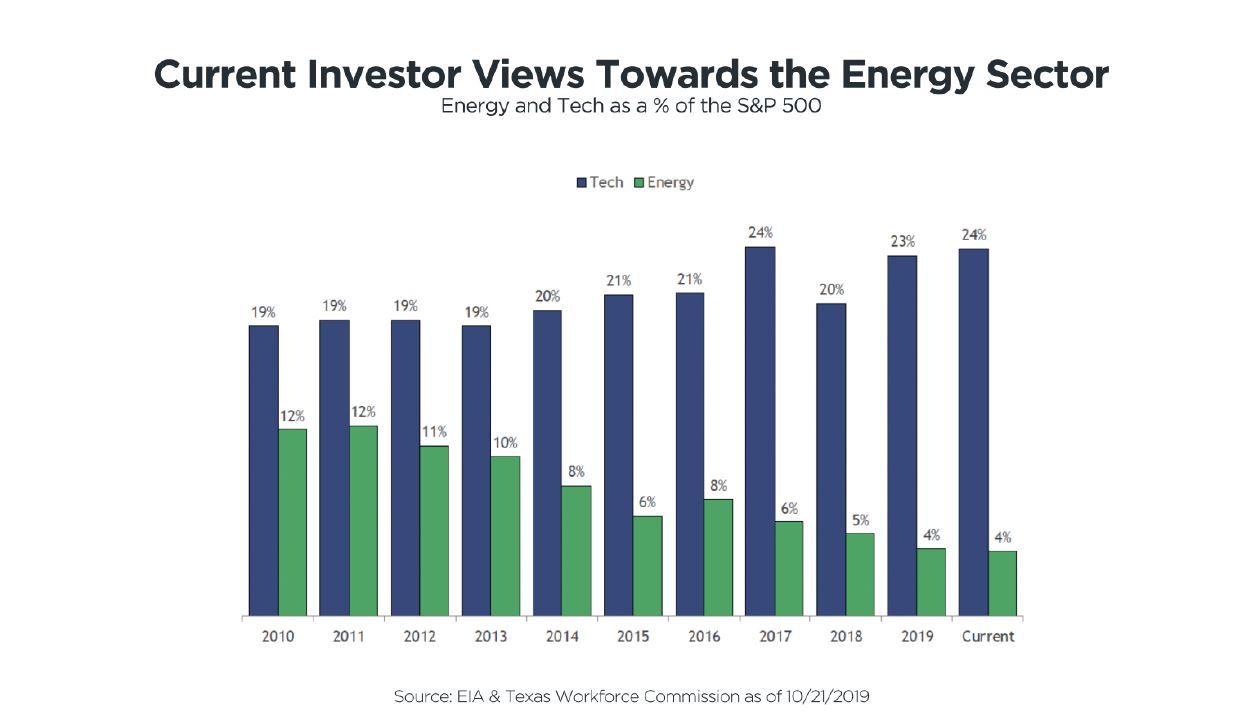

This chart plots the energy and tech sectors as a percentage of the S&P 500. The taller bars represent the tech industry, the smaller, declining green bars are the energy sector. The energy component has never been this low.

The capital providers voted with their feet.

Simultaneously, concerns have emerged around the sustainability of global oil and gas demand growth in the face of massive US shale-driven supply growth, resulting in commodity prices that make industry profitability generally poor. The industry doesn’t make much money at $50 WTI and $2.30 Nat Gas.

And to put icing on the cake, a consensus has emerged among scientists, business leaders, and the general public that climate change is a real problem that requires urgent attention from all of us, and that we therefore will be using less hydrocarbon-based energy sources.

Coupled with poor financial returns, climate change concerns have the industry dramatically out of favor at the moment, in most every corner of the investing and political world.

So, while US production will likely continue to grow, it will grow more slowly and will require less people, and will also likely be more of a “big company” game.

And most certainly, the private equity-backed new business formations that supercharged the Houston economy during this period will slow. They already have.

At the same time, while I am certainly not a climate scientist, the evidence seems compelling to me that high levels of CO2 emissions are impacting our climate. And it’s a problem that must be addressed.

And whether you individually agree with that assessment, it's hard to argue that we are not facing a dominant secular trend that has great momentum in the investment world and with the general public, and we must respond in a responsible and rational way.

At its most basic level, I think we can all agree that having less CO2 emissions in the atmosphere would be a good thing—and as Houston’s business leaders, we need to be committed to working to make that happen.

The trick, of course, is how to do that and at the same time meet the world’s energy needs.

And that is the dual challenge – meeting global energy demand while lowering the world’s carbon footprint.

How do we in Houston plan for a longer term future in which oil and gas demand eventually ceases to grow and becomes a smaller component of total global energy consumption?

It's worth pausing here to remind us that the energy industry is not our only strength in Houston. Our continuing efforts to diversify our economy and to attract and build non-energy businesses in Houston is of critical importance. Thanks to many of you in this room, we are having notable successes in this area, with more on the horizon.

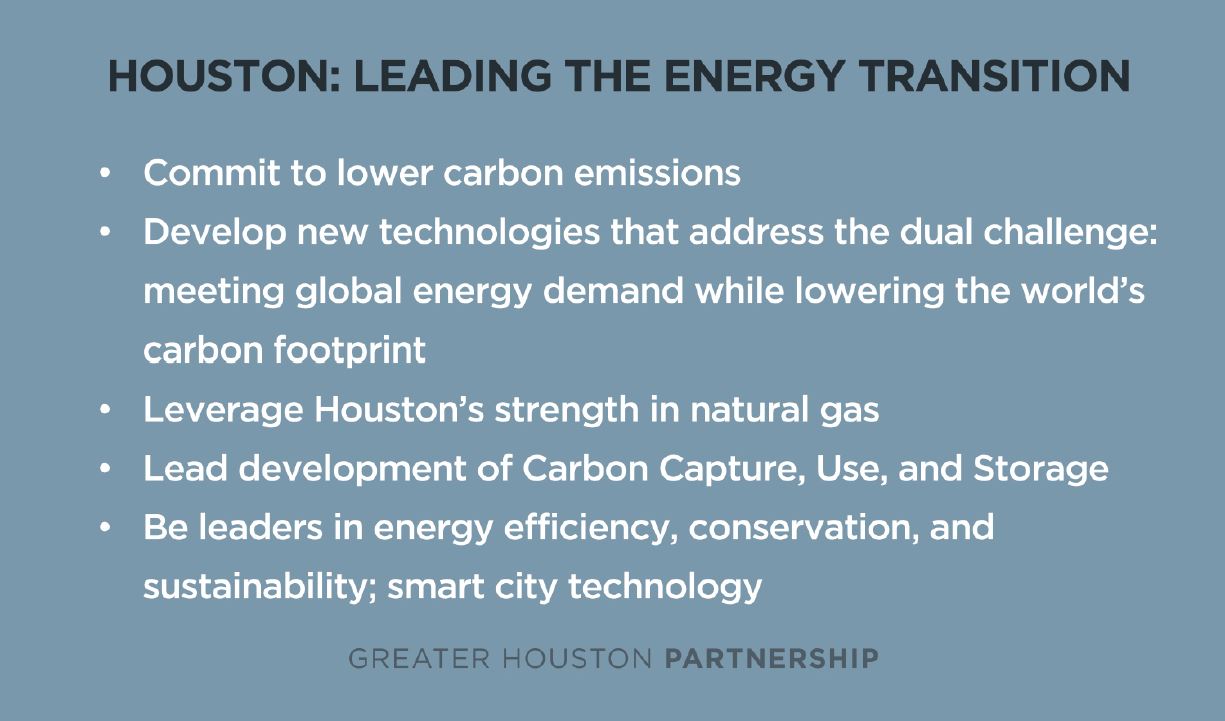

Now back to energy and my fourth point: As Houston business leaders we have a responsibility to lead the transition to a cleaner, more efficient and more sustainable lower carbon world.

So, what can we do?

For starters, we can publicly commit to lowering the carbon emissions in our own businesses. We are off to a good start in that regard, but there is much more to do.

Importantly, this is something ALL Houston businesses can do, whether you are an energy company or not. Ironically, relatively small amounts of total greenhouse gas emissions come from the core oil and gas industry; the bulk come from those businesses and individuals, including every one of us, who are consuming the hydrocarbons.

But within the energy world, committing to lowering methane emissions and drastically reducing the flaring of natural gas seems critically important and entirely doable, and it is an area where we can and must take the lead.

Second, we can put our scientific, academic, and commercial brains to work to innovate and develop new technologies that address these problems.

There are great examples of that underway in Houston, including the U of H Energy Program and Rice’s Carbon Hub.

Rice and U of H also have the #1 programs in entrepreneurship, in both graduate and undergraduate education nationally, and the new Midtown innovation district, anchored by The Ion, will include a focus on energy industry solutions.

We have 21 major corporate energy R&D centers located in Houston. Plus we are home to a range of startups focused on a broad set of technologies including blockchain, data analytics and AI.

In fact, a quarter of Houston’s VC-backed startups, are focused on energy technology.

Companies include:

Rebellion Photonics

Goexpedi

Data Gumbo

and

Incentifind

The scope of these innovations can range from smart grid technology to water recycling and reuse, to more sustainable commercial and residential building practices. We also have a growing presence of solar and wind companies who are now operating from Houston. In fact, Texas is in the national leader in wind power generation.

The cross-section of Houston's scientific community is an embedded competitive advantage:

Chemistry

Advanced Materials

Nanotechnolgy

and GEO Sciences

It is through these already established strengths that Houston can drive innovation.

Importantly, with this innovation comes fantastic economic opportunity. These companies should be a powerful new engine for growth in our region.

Third, we can leverage our strength in Natural Gas production and transportation to accelerate the transition away from coal-fired power generation and towards this cleaner burning fuel. Houston is the world capital of the Natural Gas industry, and it’s role in the future will be critical to lower global carbon emissions, both domestically and globally, especially via our LNG export businesses serving the developing world.

There will not be lower carbon emissions without natural gas being a large part of the solution.

Fourth, we can lead the charge in Carbon Capture Use and Storage technology development, also known as CCUS, which many experts believe is absolutely necessary if we are to meet the targets associated with the Paris Climate Accords, or any dramatic reduction in carbon emissions, for that matter.

While not yet economical on a large scale, the technology is promising, and could have enormous impact. The knowledge, physical infrastructure, and incentive to make that work, all sit in Houston, Texas.

And fifth, we can become outspoken leaders in the area of energy efficiency, conservation, and sustainability; along with building a leading “smart city.”

While it may feel unnatural to be advocating that people should ultimately use less of the product we sell, conservation can actually be hugely impactful in reducing carbon emissions, and there is absolutely no reason we shouldn’t be a leader in the area of energy efficiency and conservation.

The City of Houston is already the national leader as far as sourcing it’s electricity needs from sustainable sources. And The Ion Smart Cities accelerator, among other efforts, is working to build Houston into a leading smart city that extends these efficiency gains across the community.

So, where do we go from here?

As a practical matter, every member of the Partnership can contribute to the effort.

We should use our convening power, and the authority that comes with being business leaders, to rally our companies, political leaders and fellow citizens to position Houston as the city that will lead this energy transition.

The Partnership has already launched or will launch new committees to accelerate our growth in this area.

For the past year, our Energy 2.0 committee members have been working to identify and attract the key players across the new energy spectrum and we are starting to see signs of progress.

Our energy policy committee has been exploring the policy dimensions of CCUS, and will be drawing up solutions at the state and federal levels to ensure the Texas Gulf Coast is positioned as the leader in this promising new technology.

And finally, as part of a broader ‘Energy Transition’ initiative, we will think about key levers in this evolution – those key inflection points – to ensure that Houston is the leader.

There is fantastic business opportunity for us in this effort; it’s necessary and it’s the right thing to do.

Houston is about making things happen, and we can lead this energy transition. We should be driving the discussion with a seat at the table where key policy actions are being debated.

And it is not enough for us to simply educate the world on how dependent we currently are on hydrocarbon energy and how difficult it will be to change the energy mix.

While these things are both true, we can still be the voice of optimism even as we acknowledge the significance of the dual challenge.

Houston must lead the world to an era of low-cost, reliable, and climate-friendly energy. Nowhere else in the world is there such a concentration of scientists, engineers, and economists who understand energy systems and can affect the necessary change.

So let’s be the driver, not the passenger. We will get there more quickly; we will make a huge contribution to the future of humanity; and we will ensure that Houston continues to be one of the best places in the world to live, work and build a business.

Thank you very much. Have a great afternoon.

Presented:

January 22, 2020

Greater Houston Partnership Annual Meeting

Bobby Tudor

Chair, Greater Houston Partnership

Chairman, Tudor, Pickering & Holt & Co.

Stay up-to-date on what’s happening with the Partnership and Greater Houston region by opting-in to receive information on upcoming events, news, data releases and more.